At Singer Capital Markets we remain overweight the Industrials sector for now, but we think that the debate is finely balanced. On 13th February we published our first “Trend spotting” Strategy note of 2018 entitled “Synchronicity”. After severe market volatility we felt we needed to sense check the assumptions made in our Best Ideas document in January and assess if they were still intact.

Synchronised global growth

After weighing the latest evidence, our conclusion was that the global equities setback starting from the peak in the S&P 500 on 26th January was best characterised as a correction rather than a whole new phase in markets and it looks as if for now we have been correct. We also asserted that our underlying strategy for 2018 remained intact, based in part on the concept of “Synchronicity” (that is to say the phenomenon of synchronised global growth for the first time since the financial crisis of 2008/09 combined with the gradual emergence of synchronised global tightening). The evidence for synchronised global growth has continued to emerge in the course of 2018 and also for synchronised tightening – but the latter not in a way to derail the fundamentals, in our view. We therefore remained bullish on markets and also on the Industrial sector although we suggested that it was also prudent to consider whether the view on Industrials could be challenged as the year evolved.

Our note actually focused on 5 key areas:

- Macro Trends and Themes

- How our Best Ideas were performing year to date (very well as it happens)

- Some yield ideas to focus on

- Quant techniques conclusions (stick with growth and quality ideas)

- A feature on Industrial stocks

Global growth and the Industrials sector

In this blog we look just at the last very interesting area because any view or assumptions we make about global growth have the most impact on the Industrials sector and vice versa.

Below we rehearse in simple bullet form the dilemma that investors may face in this sector as the year progresses, mindful that recent market turmoil is a catalyst for people to review their holdings and that the Industrial sector is likely to be high on the list for discussion after its strong performance. Our basic stance though is to regard the current volatility as an opportunity to pick up quality Industrial names on weakness

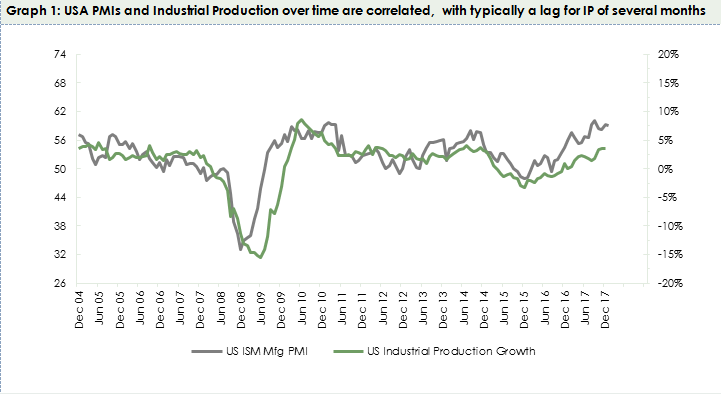

- PMI’s are still rampant, the best numbers around the world in aggregate since 2011

- PMI’s correlate closely to Industrial Production (IP) over time, but IP typically lags by around six months – download graph 1

- So IP is still going up and will be up for the whole of this year most likely, a very supportive backdrop

- However ratings are also rampant at almost 20x PE vs the long term average of 14x – download graph 2

- And PMI’s are looking toppy (the normal range is 40 – 60)

- So at some stage during the year some PMI’s are quite likely to roll over somewhat

- And traditionally the UK Industrials’ PER de-rates when US PMI’s go down

- Meanwhile currency is becoming more of a headwind than in the last two years

{kind=link}

{kind=link}

Putting this all together you can see that the far-sighted investor might start to consider at what stage our successful and ongoing overweight stance on the Industrials should be retired – watch this space for further commentary!

For more information, email enquiry@n1singer.com

Written by Mark Gibbon, Head of Research, Singer Capital Markets